More on Root Finding: The Bisection method Using Python

4 years ago

10

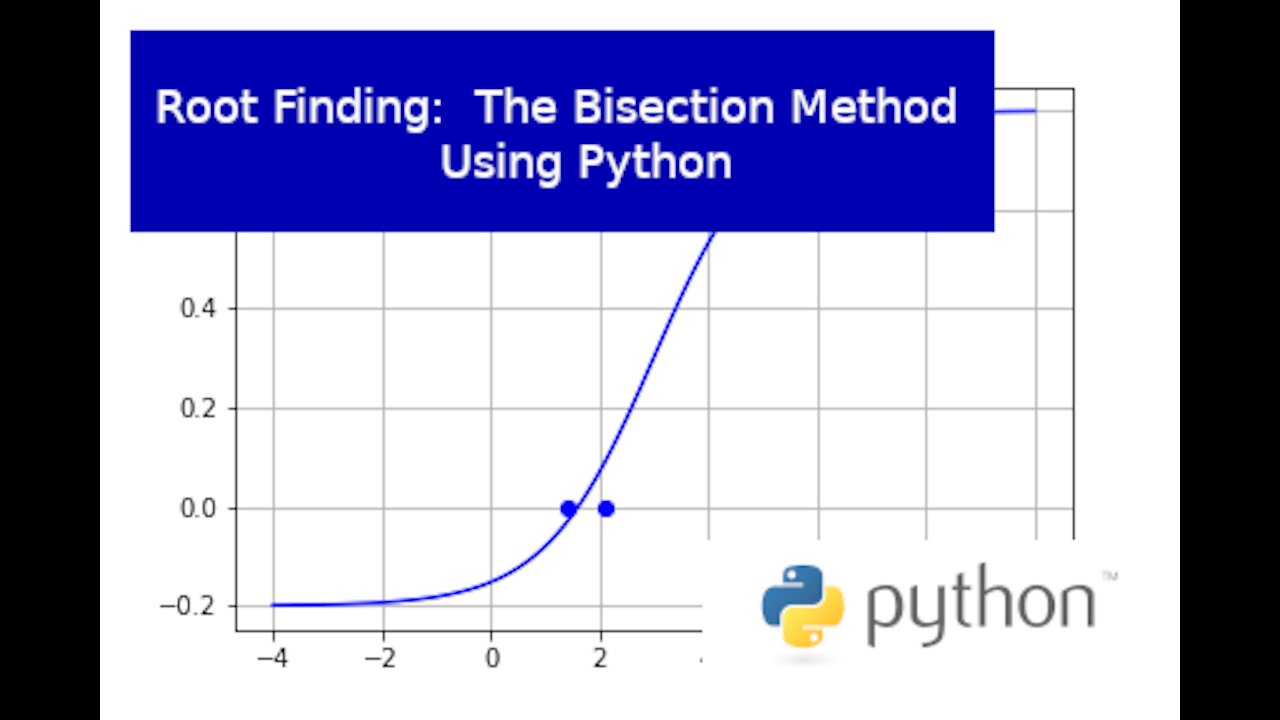

In previous videos, we have used the Newton’s method to find the roots of various functions. In particular, we inverted the Black-Scholes model to solve for the implied volatility of an option. There are, however, other algorithms that can do this. Here, I present the bisection method. This is a quick video showing the basics of the technique. I don’t go into detail with the volatility as we have done that in several previous videos.

Troubleshooting Newton’s mMethod: https://youtu.be/Q6COHive9CY

Original IV Video: https://youtu.be/Jpy3iCsijIU

Github: https://github.com/kpmooney/numerical_methods_youtube/tree/master/root_finding/bisection

Tip Jar: http://paypal.me/kpmooney

Loading comments...

-

14:31

14:31

kpmooney

4 years ago $0.01 earnedScipy's built-in root finding function: Solve nonlinear equations with Python

33 -

7:52

7:52

monsterMatt

5 years agoPython Importing and Using Classes

192 -

9:23

9:23

GannJourneyman

4 years ago $0.02 earnedUsing the Gann Equinox Squaring Method

104 -

17:21

17:21

kpmooney

4 years agoLinear Regression in Python: Finding a Stock's Beta Coefficient

34 -

2:22

2:22

Age of Discovery

4 years ago $0.02 earnedUsing Python and Notepad++ for Reality Programming

186 -

21:36

21:36

kpmooney

4 years agoMore Kinematics problems: Differential Equations and Event Detection using Python (Numpy and Scipy)

37 -

6:51

6:51

Affiliate Marketing Training

5 years ago $0.01 earnedVisualize your reality by using this method!!

110 -

4:56

4:56

monsterMatt

5 years agoImporting and Using Custom Classes in Python

114 -

21:36

21:36

kpmooney

4 years agoCalculating Implied Volatility from an Option Price Using Python

134 -

11:24

11:24

kpmooney

4 years agoCalculating the Implied Volatility of a Put Option Using Python

10